The Federal Reserve is expected to leave its target rate unchanged at tomorrow’s policy meeting, marking a shift after three straight cuts in 2025. Keeping rates steady is the current outlook until June, but several factors are in play that could change the calculus in the weeks ahead.

Let’s start with what appears likely: the Fed funds futures market is pricing in a high probability that the central bank will keep its target rate steady at a 3.5%-to-3.75% range at tomorrow’s FOMC meeting.

The policy-sensitive 2-year Treasury yield is aligned with the no-change outlook. The difference between this widely-followed yield and the current effective Fed funds (EFF) rate is close to the smallest spread in nearly a year. That’s a sign that this slice of the Treasury market is no longer anticipating rate cuts, which was the case in previous months, when the 2-year yield traded well below EFF – falling below -80 basis points at one point last May.

As always, the outlook turns increasingly cloudy the further beyond the next FOMC meeting we look, but a host of conflicting factors make looking ahead unusually challenging.

One source for thinking that the Fed will be hard pressed to cut rates anytime soon: US economic activity has remained resilient, which suggests that easing policy further is unnecessary if not inflationary.

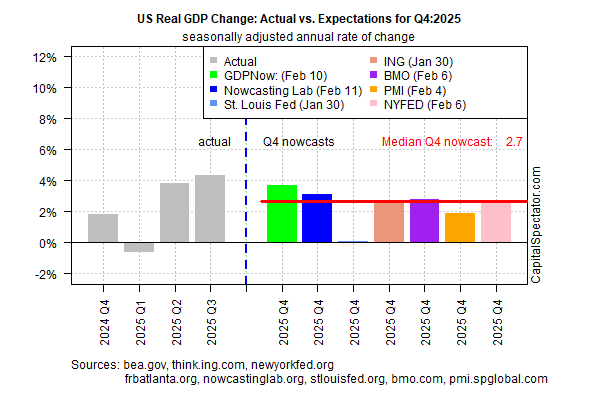

Although some economists last year warned that recession risk was rising, recent nowcasts for the upcoming (and delayed) fourth-quarter GDP report are pointing to ongoing strength. The Atlanta Fed’s GDPNow model is currently nowcasting that Q4 growth will accelerate to 5.4%, which (if correct) would mark the highest output in four years.

Analysts warn that developing relatively reliable Q4 nowcasts is still challenging because of the lingering effects from the government shutdown in October. But as The Capital Spectator reported last week, taking a more cautious view of Q4 nowcasts, by using a median estimate from several sources, still points to a relatively robust, if slower economy in the final three months of 2025. On that basis, there’s arguabbly still a case for going slow with policy changes, if not pausing rate cuts.

Peter Hooper, vice chair of research at Deutsche Bank, agrees. “It’s time to sit back and take a look at things,” he tells The New York Times. “We will get some further easing, but it’s not urgent at this point.”

The counterview is that inflation, for all the concern surrounding a tariff-driven shock, remains relatively stable, which in turn leaves room for more rate cuts, if only as insurance to keep the economy humming. Last week’s delayed update of November’s personal consumption expenditures price index – the Fed’s preferred measure of inflation – ticked up to a 2.8% year-over-year pace for headline and core readings. That’s up from 2.7% in October, and slightly further above the Fed’s 2% target.

The Richmond Fed’s analysis of the latest monthly PCE numbers in context with the historical record, however, suggest that “inflation is behaving as it did prior to the pandemic, in a manner broadly consistent with — or slightly below — the Fed’s 2 percent target.”

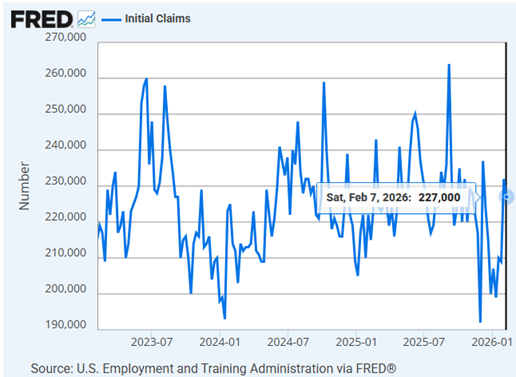

Meanwhile, the jury’s still out on whether the recent updates showing a slowdown in hiring is sign of a broader economic slowdown in progress. Some economists say that the marked downshift in payrolls growth warrants more rate cuts. The pushback is that softer hiring has yet to translate to a rise in layoffs, as indicated by the low level of jobless claims in recent months.

Adding to the Fed’s challenge of setting rates in a complex macro environment is the ongoing political pressure from the White House to ease policy further. President Trump last week renewed his criticism of Fed Chair Jerome Powell and told CNBC that inflation had been “defeated.”

Perhaps the Fed’s biggest challenge is persuading markets that, whatever the central bank decides in the months ahead, it’s setting rates based on independent analysis of the economy. That’s getting harder at a time of an ongoing criminal investigation of Fed Governor Lisa Cook, which some observers say is a thinly-veiled effort by the White House to influence the central bank’s decisions in favor of more rate cuts by opening up a new seat at the Fed.

Further roiling the outlook: Powell’s tenure as Fed chair ends in May, and it’s unclear how a new Fed chair would influence policy.

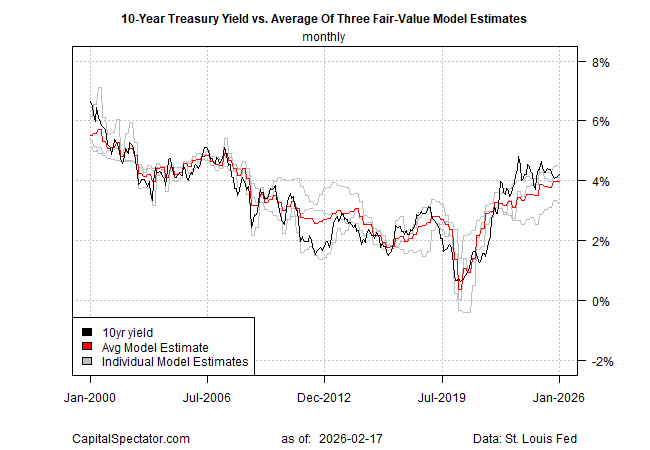

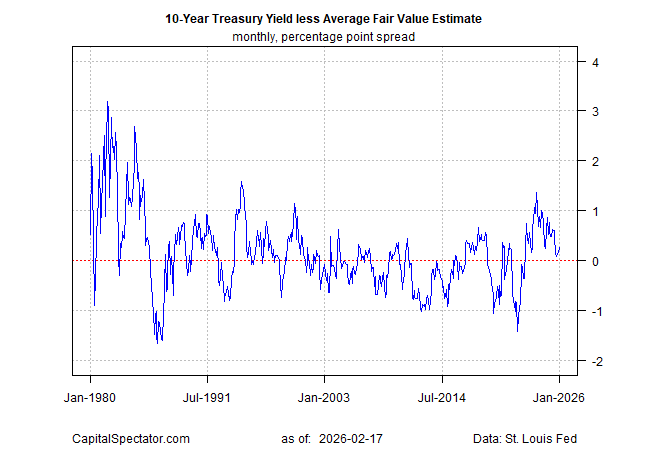

So far, however, the Treasury market appears relatively calm, and so it can be argued that the crowd isn’t particularly worried. The benchmark 10-year yield, although it’s increased lately to the highest level since August a few days ago, is still trading at a middling range vs. recent history.

A rise in this key yield above its recent trading range could change the calculus, perhaps dramatically. All the more so at a time of growing concern about government debt around the world.

The rise of gold above $5000 an ounce this week highlights the growing concerns related to the so-called debasement.

“We’re at the start of a global debt crisis, with markets increasingly fearful governments will attempt to inflate away out-of-control debt,” wrote Robin Brooks, a senior fellow at the Brookings Institution and former chief economist at the Institute of International Finance.

For now, at least, the Treasury market has yet to signal trouble ahead in the form of persistently rising yields. When and if that changes, the risk calculus will change. The challenge of the moment is deciding if this is the calm before the storm, or just another round of noise driven by overbaked warnings.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}